Business Plan for Bank Loan in Nigeria requirements are becoming more detailed in 2026 as banks tighten risk assessments and prioritize financially structured businesses. Entrepreneurs seeking loans from CBN licensed banks are discovering that a simple idea is no longer enough. Financial institutions now expect clear documentation, realistic projections, operational planning, and evidence that the business can survive economic uncertainty.

- Cash flow stability

- Profitability forecasts

- Business registration status

- Risk management systems

- Market demand

- Founder credibility

- Operational structure

This guide explains what modern lenders expect, common mistakes entrepreneurs make, and how to build a stronger Business Plan for Bank Loan in Nigeria applications.

Why Business Plan for Bank Loan in Nigeria Requirements Matter More in 2026

Many entrepreneurs assume banks only care about collateral. While collateral remains important, lenders increasingly evaluate whether businesses are operationally sustainable.

According to guidance and financial stability policies from the Central Bank of Nigeria (CBN), financial institutions continue strengthening risk assessment standards for commercial lending.

This means banks want evidence that:

- The business understands its market

- Revenue projections are realistic

- Operational systems exist

- Risks are properly managed

- The founder understands financial planning

A weak or unrealistic business plan often signals poor management preparation. A properly structured Business Plan for Bank Loan in Nigeria application improves lender confidence significantly.

What CBN Licensed Banks Usually Expect

Most commercial banks in Nigeria now expect business plans to contain both strategic and financial clarity.

Typical expectations include:

- Executive summary

- Business description

- Market analysis

- Revenue model

- Financial projections

- Operational structure

- Marketing strategy

- Risk analysis

- Cash flow forecasts

- Loan repayment strategy

The goal is simple: banks want confidence that the business can repay the loan responsibly.

Business Plan for Bank Loan in Nigeria Must Be Realistic

One major reason many loan applications fail is unrealistic forecasting.

For example, some entrepreneurs project:

- Massive profits within a few months

- Rapid nationwide expansion immediately

- Unverified customer demand

- Unclear operational costs

Experienced loan officers can usually identify unrealistic assumptions quickly.

Instead of exaggerated projections, banks prefer:

- Conservative estimates

- Clear operational planning

- Transparent cost calculations

- Evidence-based market research

Realistic planning builds credibility. Every strong Business Plan for Bank Loan in Nigeria should balance ambition with realistic operational forecasting.

Why Cash Flow Matters in a Business Plan for Bank Loan in Nigeria

Many businesses appear profitable on paper but struggle with cash flow problems.

In 2026, banks are paying closer attention to how businesses manage operational cash movement.

For example:

- How quickly customers pay invoices

- Inventory turnover speed

- Supplier payment cycles

- Monthly operating expenses

- Currency exchange risks

Businesses that cannot explain their cash flow clearly often appear financially unstable. This is why Business Plan for Bank Loan in Nigeria documentation now requires more detailed financial explanations.

This related guide explains how many African businesses now calculate profitability more accurately: How to Calculate Business Profit in Africa (Including Hidden Costs, FX & Logistics 2026).

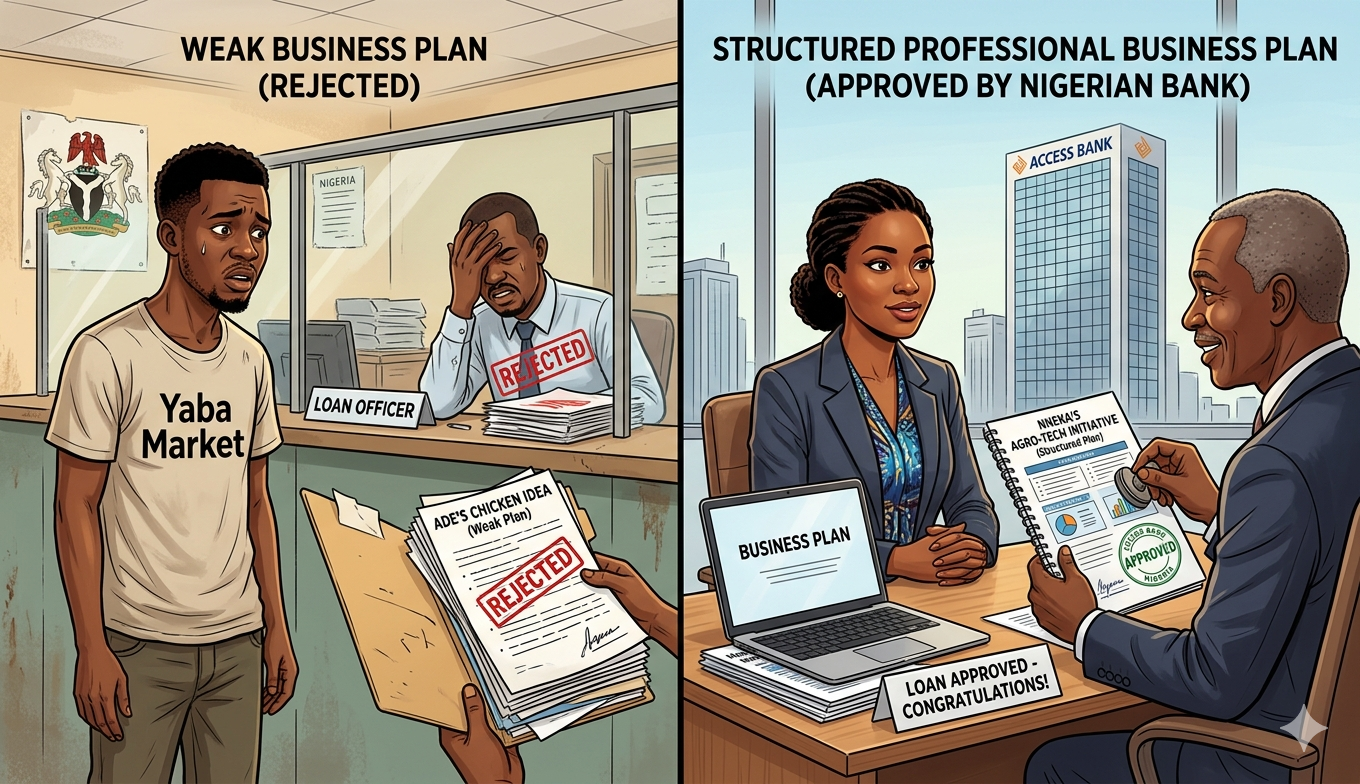

Realistic Example: Food Processing Startup in Abuja

Consider a realistic scenario.

A small food processing startup in Abuja applied for expansion funding in 2025. Initially, the founder submitted a short business proposal with ambitious revenue claims but limited operational detail.

The bank rejected the application.

After consulting financial advisors, the founder rebuilt the Business Plan for Bank Loan in Nigeria submission with:

- Detailed production costs

- Supplier agreements

- Market demand analysis

- Inventory planning

- Monthly cash flow projections

- Risk management systems

The revised application demonstrated stronger financial discipline and eventually secured financing.

The difference was not just the idea. It was the structure and credibility of the plan.

Why Proper Business Registration Matters

Banks generally prefer dealing with properly registered businesses.

Formal registration demonstrates:

- Operational legitimacy

- Regulatory compliance

- Long-term business commitment

- Better accountability

Entrepreneurs launching businesses in Nigeria should understand CAC registration costs, hidden fees, and processing timelines before seeking funding.

This guide explains the details: Company Registration Cost in Nigeria (2026): Hidden Fees, CAC Charges & Processing Time.

Why Market Research Strengthens Loan Approval

Banks want evidence that customers actually need the product or service.

Strong market research often includes:

- Industry demand trends

- Competitor analysis

- Target customer behavior

- Pricing research

- Growth opportunities

For example, an entrepreneur opening a logistics business in Lagos should understand:

- Delivery demand trends

- Traffic-related operational costs

- Competition levels

- Fuel cost fluctuations

- Technology adoption trends

Specific market understanding increases lender confidence.

Digital Assets and Modern Loan Credibility

In 2026, many lenders increasingly evaluate a business’s digital presence.

Businesses with:

- Professional websites

- Strong branding

- Customer engagement systems

- Social proof

- Online visibility

often appear more organized and scalable.

This is why many entrepreneurs are moving beyond short-term online income methods and focusing on building long-term digital assets such as:

- Websites and blogs

- YouTube channels

- Mobile apps

- Email subscriber systems

- Niche content platforms

Small online earning methods can help beginners learn valuable skills, but sustainable business growth usually requires scalable infrastructure.

Some growth-focused teams such as Valspill Team now help businesses develop these digital systems properly for long-term revenue and operational visibility.

The Growth Path Banks Prefer to See

Most financial institutions prefer businesses showing gradual, realistic growth progression.

Typical sustainable business growth often follows this pattern:

- Learning Stage — Understanding the market and customer demand

- Operational Stage — Building stable revenue systems

- Digital Asset Stage — Developing online infrastructure

- Automation Stage — Improving operational efficiency

- Scaling Stage — Expanding with structured financial planning

Banks generally trust businesses more when they show operational maturity instead of unrealistic overnight success expectations.

How Trademark Protection Supports Loan Applications

Brand protection may also improve business credibility.

Businesses that secure trademarks often appear more serious about long-term growth and market positioning.

Trademark protection also reduces risks related to brand imitation and disputes.

This guide explains the process: Protect Business Name in Nigeria (Trademark Registration Guide 2026/2027).

Insurance and Risk Management Expectations

Risk management is becoming increasingly important in commercial lending.

Banks often evaluate whether businesses are prepared for:

- Operational disruptions

- Inventory losses

- Equipment damage

- Liability risks

- Unexpected financial pressure

Businesses with insurance coverage may appear more financially responsible.

This related guide explores SME insurance options: SME Business Insurance in Nigeria (Best Coverage Options in Africa 2026/2027).

Franchise vs Licensing Business Models

The type of business structure also affects how lenders assess risk.

For example, franchise businesses sometimes appear lower-risk because they operate under established systems and brand recognition.

Licensing models may offer greater flexibility but can require stronger operational execution.

This guide compares both approaches in detail: Franchise vs Licensing In Africa: Which Business Model Is More Profitable in 2027?.

How Entrepreneur Burnout Affects Loan Performance

Banks increasingly recognize that founder stability affects business sustainability.

Entrepreneurs handling every operational task alone may struggle with:

- Decision fatigue

- Operational inconsistency

- Poor financial management

- Delayed customer support

- Growth stagnation

This is one reason many modern businesses now use automation and AI systems to reduce operational stress.

This related guide explains how AI tools are helping solo founders build more sustainable businesses: Entrepreneur Burnout Solo Founders (Why AI Co-Founders Change Everything in 2026).

Common Mistakes That Hurt Loan Applications

Several avoidable mistakes reduce approval chances significantly.

1. Unrealistic Revenue Projections

Exaggerated profit expectations often reduce credibility.

2. Weak Financial Documentation

Missing expense breakdowns and unclear cash flow create risk concerns.

3. Poor Market Understanding

Businesses must understand their industry and competitors clearly.

4. Lack of Operational Planning

Banks want to know how the business will function daily.

5. No Repayment Strategy

Every Business Plan for Bank Loan in Nigeria should clearly explain how the loan will be repaid.

Practical Tips for Writing a Strong Business Plan for Bank Loan in Nigeria

Entrepreneurs can improve loan approval chances by:

- Using realistic financial assumptions

- Including accurate operational costs

- Providing evidence-based market research

- Explaining customer acquisition strategies

- Showing strong organizational systems

- Demonstrating repayment planning

- Maintaining clear formatting and structure

Clarity and professionalism matter. A detailed Business Plan for Bank Loan in Nigeria presentation can improve approval chances and strengthen business credibility.

The Future of Business Financing in Nigeria

Commercial lending is evolving rapidly.

In 2026 and beyond, businesses will likely need:

- Stronger digital visibility

- Better financial reporting

- Improved operational systems

- Smarter automation

- More transparent profitability tracking

Entrepreneurs who build organized systems early may find it easier to access funding opportunities later.

Final Thoughts

Business Plan for Bank Loan in Nigeria preparation is no longer simply about writing a document. In 2026, banks expect operational clarity, financial realism, and evidence that the business can survive competitive market conditions.

Small online income methods and beginner side hustles may help entrepreneurs learn valuable skills, but sustainable financial growth usually comes from building scalable businesses and structured systems.

The businesses most likely to secure long-term funding are often those with:

- Strong operational planning

- Accurate financial visibility

- Professional digital presence

- Scalable infrastructure

- Responsible risk management

If you are planning to apply for business financing in Nigeria, this may be the right time to move beyond basic proposals and start building a business structure designed for long-term sustainability.

Frequently Asked Questions (FAQ)

What should a Business Plan for Bank Loan in Nigeria include?

A strong business plan should include an executive summary, market analysis, financial projections, operational structure, repayment strategy, and risk management details.

Do Nigerian banks require registered businesses for loans?

Most banks prefer properly registered businesses because registration improves legal credibility and operational transparency.

Why do banks reject business loan applications?

Common reasons include unrealistic projections, weak financial records, poor cash flow planning, and unclear repayment strategies.

Can digital businesses qualify for bank loans?

Yes. Many digital businesses qualify if they demonstrate consistent revenue, operational systems, and realistic financial planning.

Are small online side hustles enough for long-term business growth?

Usually not alone. They can help entrepreneurs gain experience, but scalable digital assets and operational systems typically provide more sustainable growth.

How can entrepreneurs improve loan approval chances?

Entrepreneurs can improve approval chances by maintaining accurate records, building realistic projections, improving operational systems, and presenting professionally structured business plans.