A successful business loan application is not simply about presenting profit figures or submitting a stack of financial documents. In 2026, banks in Nigeria and across the world are becoming far more cautious about lending money to small businesses. They want evidence that your business can survive economic pressure, maintain stable cash flow, and repay consistently over time.

This is why many entrepreneurs feel frustrated after loan rejection. They believe their business is profitable enough, yet banks quietly evaluate factors most business owners never fully understand.

The truth is simple: lenders are not only funding ideas. They are funding structure, discipline, consistency, and long-term survival potential.

Understanding how banks assess a business loan application can significantly improve your chances of approval while helping you build a more sustainable business overall.

Why Most Business Loan Applications Get Rejected

According to reports from the Central Bank of Nigeria (CBN) and SME-focused financial institutions, thousands of small businesses apply for funding yearly, yet many are denied.

Interestingly, rejection often has little to do with whether the business idea itself is good.

Banks are primarily asking one question:

“Can this business reliably repay the loan without creating unnecessary risk?”

If the answer appears uncertain, approval becomes difficult.

Here are common reasons many business loan applications fail:

- Inconsistent cash flow

- Poor bookkeeping records

- Mixing personal and business finances

- Weak transaction history

- Unclear business structure

- Lack of digital credibility

- Overdependence on one customer or income source

Many entrepreneurs focus only on profits while ignoring operational signals banks quietly analyze behind the scenes.

Cash Flow Matters More Than Profit

One of the biggest secrets about a business loan application is that banks care more about cash flow consistency than large revenue numbers.

A business may show impressive sales during certain months but still appear risky if inflows fluctuate heavily.

For example:

- A boutique making ₦4 million in December but struggling for the next three months appears unstable.

- A smaller grocery business generating steady weekly transactions may actually look safer to lenders.

Banks analyze:

- Average monthly inflow

- Transaction consistency

- Expense behavior

- Repayment history

- Average account balance

- Financial discipline during slow seasons

This explains why some small businesses get approved quickly while larger businesses face rejection.

you can read more about:

| WhatsApp to E-Commerce Store: What Happened When I Moved My Small Business Online |

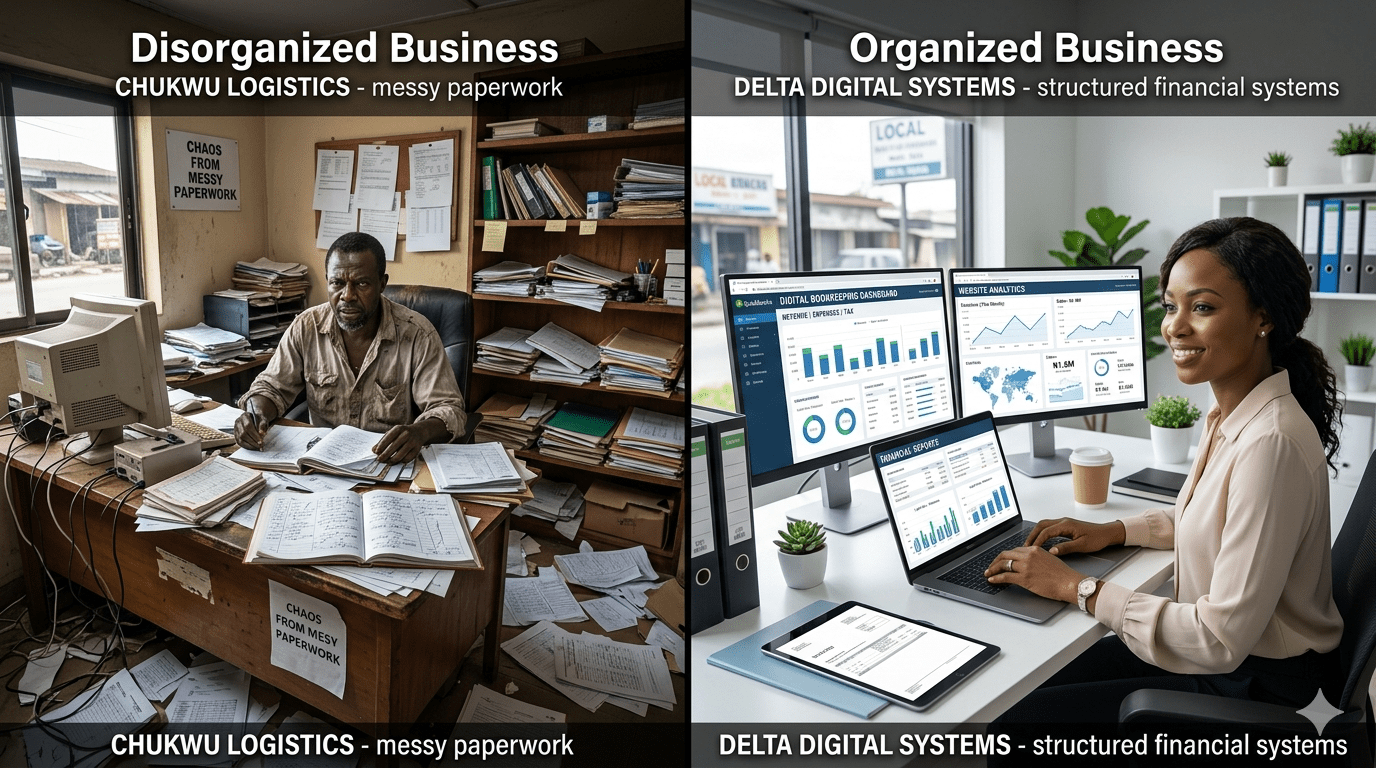

The Financial Mistake Many Entrepreneurs Make

Many bootstrapped businesses start informally, which is understandable. Entrepreneurs often use personal accounts to receive payments and manage expenses in the early stages.

The problem begins when this continues long-term.

One major red flag in a business loan application is mixing personal and business finances.

For instance:

- Paying rent from business funds

- Using customer payments for personal shopping

- Frequent unrelated transfers

- Random cash withdrawals

When lenders review account statements and notice these patterns, it becomes harder to evaluate the actual financial health of the business.

Businesses that survive beyond year three usually create clear financial systems early.

What Banks Quietly Look For Beyond Your Documents

Many accountants help businesses prepare tax reports and financial statements, but lenders often evaluate operational behavior just as much as paperwork.

Here are some hidden factors banks consider during a business loan application.

1. Stability of Customer Activity

Banks prefer businesses with repeat customers and predictable demand.

If revenue depends entirely on one customer or seasonal spikes, lenders may see higher risk.

2. Business Visibility and Credibility

In 2026, online visibility matters more than many entrepreneurs realize.

Banks increasingly check:

- Business websites

- Google presence

- Customer reviews

- Social media activity

- Professional branding

A business with no online presence may appear less credible, even if sales are strong offline.

3. Operational Structure

Businesses with organized systems appear safer to lenders.

Examples include:

- Digital invoicing

- Inventory tracking

- Payroll records

- Documented expenses

- Automated payment systems

These systems demonstrate professionalism and financial discipline.

Why Bootstrapped Businesses Often Fail Before Year Three

Bootstrapped businesses rely heavily on personal savings or reinvested profits instead of external funding.

While this approach reduces debt initially, it also creates pressure.

Many businesses collapse because they:

- Operate without emergency reserves

- Scale too aggressively

- Ignore documentation

- Lack customer retention systems

- Depend entirely on physical sales

- Have no digital assets

The businesses that survive usually think beyond daily income.

They focus on systems that continue generating opportunities long-term.

What Successful Businesses Did Differently

They Built Predictable Systems

Strong businesses rarely rely on luck alone.

Successful entrepreneurs create systems for:

- sales tracking,

- customer follow-up,

- inventory management,

- content marketing,

- and revenue monitoring.

This makes the business more stable and attractive during a business loan application.

They Diversified Their Revenue Sources

Many resilient businesses learned not to rely on a single income stream.

For example:

- A fashion brand may sell products online and offline

- A consultant may combine services with online courses

- A creator may monetize ads, affiliates, and sponsorships

Diversification improves business survival during economic changes.

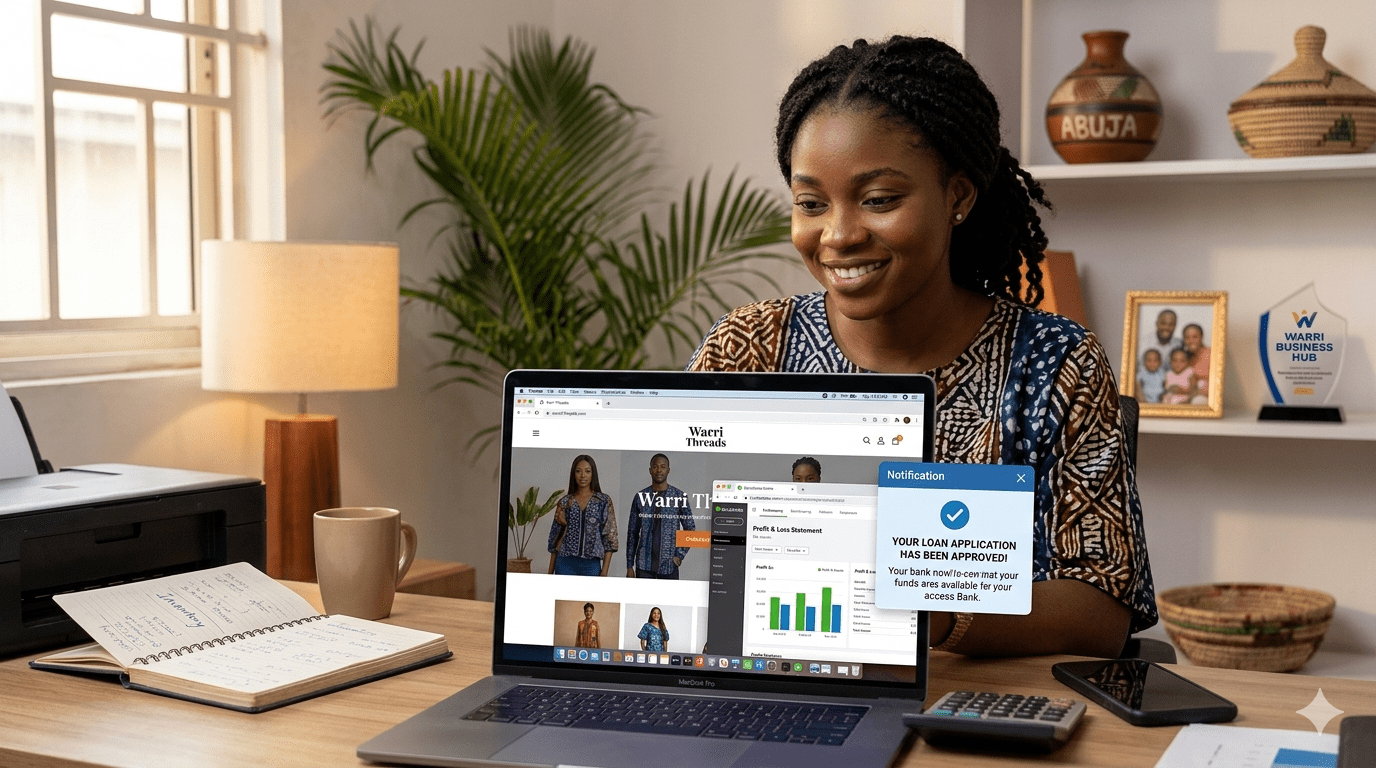

They Invested in Digital Assets

This is one of the biggest differences between struggling businesses and scalable businesses in 2026.

Digital assets continue working even when the owner is offline.

Examples include:

- Websites

- Blogs

- YouTube channels

- Email lists

- Mobile apps

- Online communities

The Valspill team develops and structures these digital assets properly for long-term traffic, monetization, and scalable business growth.

The Reality About Small Online Earning Methods

Many people start their online journey using:

- microtask apps,

- survey platforms,

- small freelancing gigs,

- or reward-based earning apps.

These methods can help beginners learn digital skills and generate starter income, but they usually have income limitations.

Long-term financial growth typically comes from building assets you control.

This is the common growth path:

Small Income Methods → Skill Development → Digital Asset Building → Scalable Revenue

For example:

- A freelancer starts writing online

- The content begins ranking on search engines

- Traffic grows steadily

- The website generates advertising and affiliate income

- The audience becomes a business ecosystem

This is why many entrepreneurs are shifting toward content-driven business models.

Case Study: Two Businesses Applying for the Same Loan

Business A

- No business website

- Manual records only

- Personal and business funds mixed

- Irregular transaction patterns

- No customer retention strategy

Result:

The lender sees uncertainty and repayment risk.

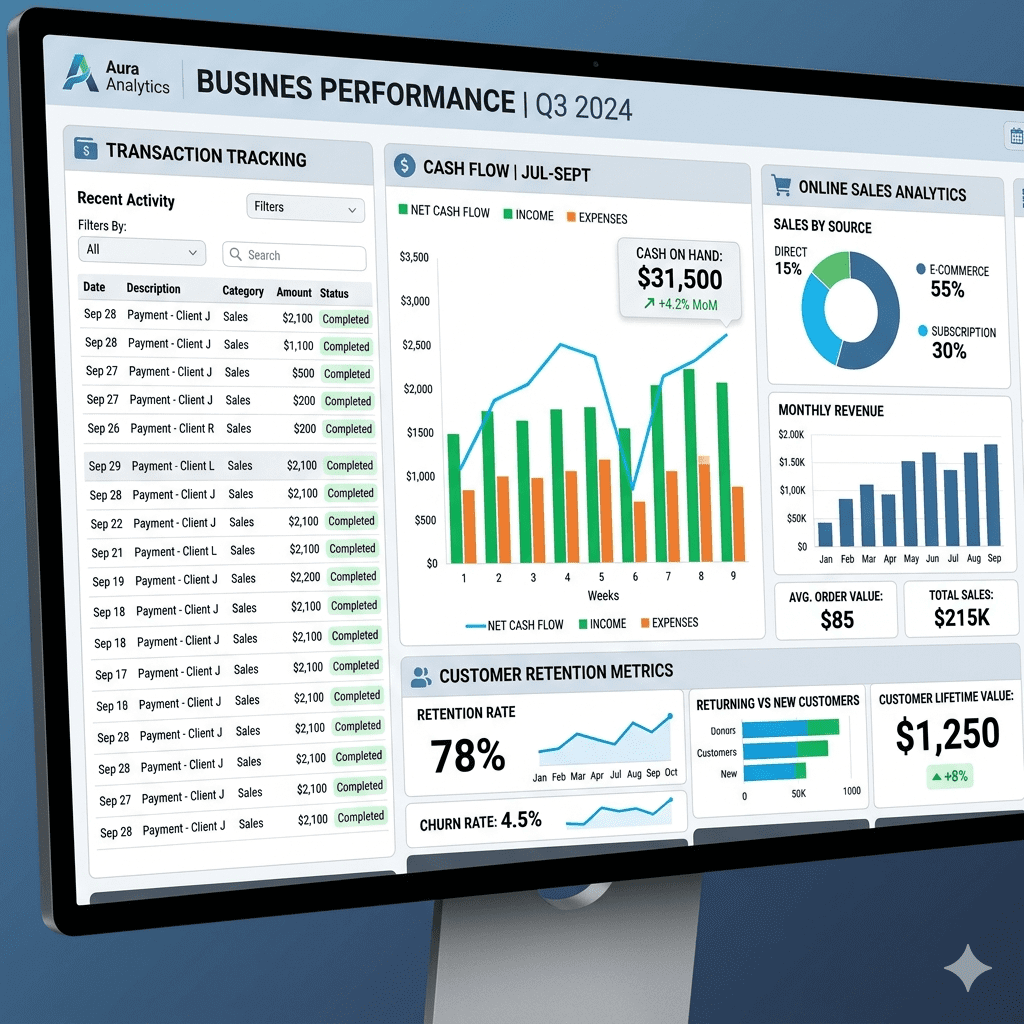

Business B

- Professional website

- Digital bookkeeping

- Consistent monthly inflow

- Structured branding

- Multiple customer channels

- Strong online visibility

Result:

The business appears more stable, scalable, and trustworthy during the business loan application review process.

How to Strengthen Your Business Loan Application in 2026

If you plan to apply for business funding, focus on improving these areas first:

- Maintain separate business accounts

- Track every transaction properly

- Build consistent monthly inflow

- Create professional online visibility

- Develop digital assets

- Improve customer retention

- Reduce unnecessary financial chaos

Small operational improvements often create major long-term advantages.

FAQ

What is the most important part of a business loan application?

Cash flow consistency is one of the biggest factors banks evaluate because it shows repayment stability.

Can a small business get approved for a loan in Nigeria?

Yes. Many lenders support SMEs, but businesses with proper records and financial structure usually perform better during evaluation.

Does a business website help loan approval?

Yes. A professional website improves credibility, online visibility, and customer trust, which can strengthen a business loan application.

Why do many bootstrapped businesses fail early?

Many struggle with inconsistent cash flow, lack of structure, poor documentation, and overdependence on a single revenue source.

Are online earning apps enough for long-term financial growth?

Not usually. They can help beginners start earning, but scalable income often comes from building digital assets such as blogs, websites, apps, or content platforms.

Final Thoughts

A strong business loan application is not built overnight.

Banks want to see more than ambition. They want proof that your business can survive, adapt, and operate responsibly over time.

The businesses that succeed long-term usually focus on structure instead of appearances.

They build systems.

They track finances properly.

They invest in digital visibility.

They create assets that continue generating opportunities even during difficult economic periods.

Small earning methods can be useful starting points, but sustainable growth often comes from building scalable systems around traffic, content, and digital ownership.

If you are serious about long-term business growth, learning how to combine operational discipline with digital assets may become one of the smartest decisions you make in 2026 and beyond.