SME Loan Platforms In Africa are transforming how entrepreneurs raise business capital in 2026. Across Nigeria, Kenya, South Africa, Ghana, and other fast-growing African economies, small business owners are increasingly turning to fintech lenders instead of traditional banks for faster approvals, lower paperwork requirements, and more flexible repayment systems.

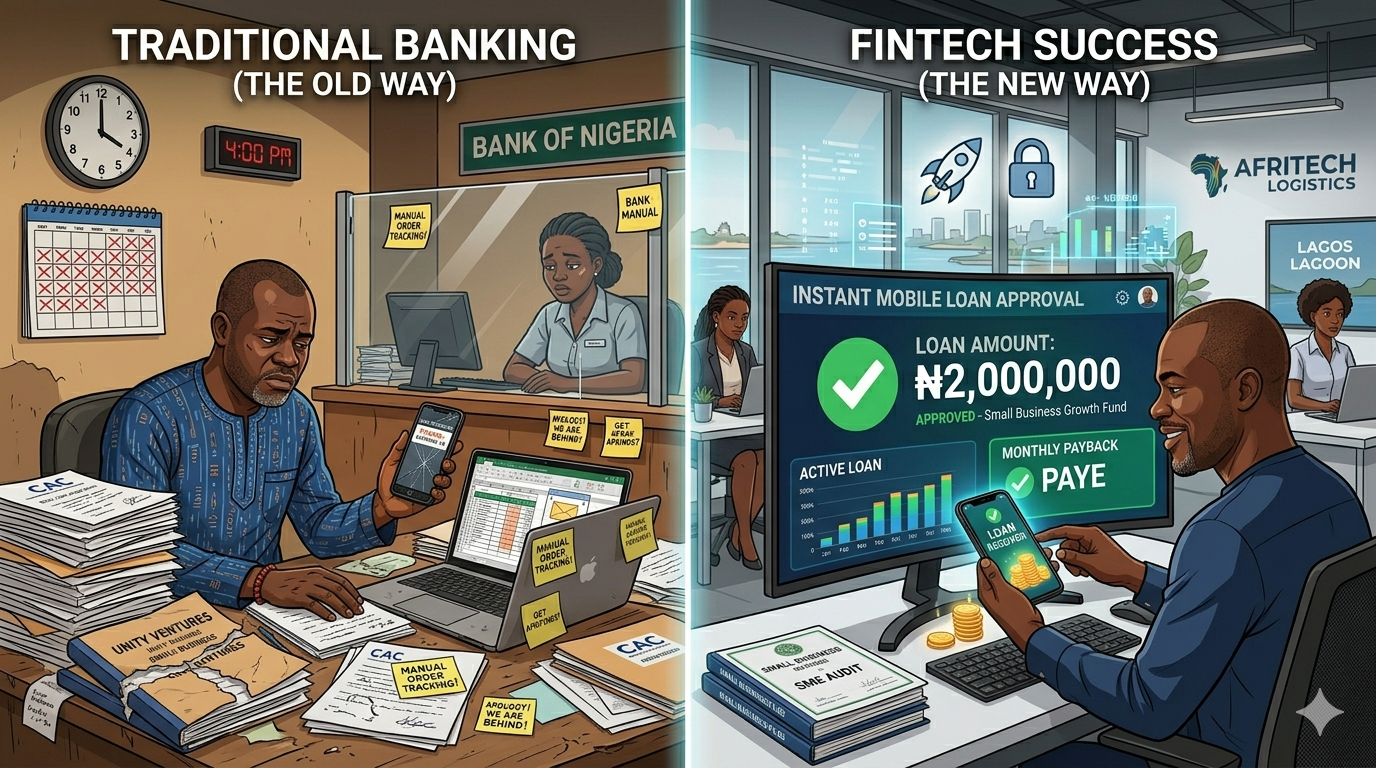

For many entrepreneurs, accessing business funding through banks remains difficult. High collateral demands, slow approval timelines, strict documentation rules, and limited support for informal businesses continue to block thousands of SMEs from securing growth capital.

This is why SME Loan Platforms In Africa are growing rapidly.

Digital lenders now use alternative credit scoring systems powered by transaction history, mobile money activity, e-commerce sales, POS records, and business cash flow patterns. Instead of waiting months for approvals, some SMEs can now receive financing within hours or days.

Still, there is an important reality many entrepreneurs overlook:

Not every SME loan is good for business growth.

Some lenders advertise low-interest financing while hiding expensive repayment structures inside processing fees, rollover systems, and short repayment cycles. Others genuinely help businesses grow responsibly with transparent funding systems.

This detailed guide compares the best SME Loan Platforms In Africa, explains how fintech business lending works in 2026, highlights realistic borrowing expectations, and shows how entrepreneurs can transition from dependency on small loans toward building scalable digital income systems.

Why SME Loan Platforms In Africa Are Growing So Fast

The growth of SME Loan Platforms In Africa is directly connected to the continent’s rising digital economy.

Millions of African businesses now operate through:

- Mobile payments

- WhatsApp commerce

- Online stores

- POS systems

- Social media sales

- Digital banking apps

This creates valuable transaction data that fintech companies can use to assess borrower risk.

Unlike traditional banks that may focus heavily on collateral or long operating history, modern SME Loan Platforms In Africa often analyze:

- Revenue consistency

- Business cash flow

- Inventory movement

- Customer payment patterns

- Digital transaction volume

- Bank statement activity

According to the African Development Bank, the SME financing gap across Africa remains enormous, leaving fintech lenders with significant growth opportunities.

As a result, competition among digital lenders is increasing, which is helping improve financing access for small businesses.

Best SME Loan Platforms In Africa 2026 Compared

The best SME Loan Platforms In Africa now offer faster approvals, easier applications, and flexible repayment options designed for growing businesses. However, entrepreneurs should still compare loan terms carefully because low monthly rates can sometimes hide expensive total repayment costs.

1. FairMoney Business Loans (Nigeria)

FairMoney remains one of the most recognized fintech lenders in Nigeria in 2026.

The platform provides:

- Quick business loans

- Automated loan approvals

- Mobile-based applications

- Flexible SME financing

Many Nigerian entrepreneurs prefer FairMoney because applications can be completed directly through smartphones without visiting physical branches.

Best suited for:

- Retail traders

- E-commerce sellers

- Service businesses

- Inventory financing

However, business owners should still review repayment schedules carefully before accepting funding.

If you are preparing for formal financing in Nigeria, this guide on Business Bank Account Nigeria Documents: The Complete Guide You Must Know in 2026 explains the key documents many lenders now require.

2. Branch International

Branch operates across several African countries and continues expanding its SME lending products in 2026.

The company uses smartphone-based behavioral analysis and transaction activity for credit evaluation.

Advantages include:

- Fast application systems

- Low paperwork requirements

- Accessible mobile financing

- Small business flexibility

Potential concern: Repeated short-term borrowing can become expensive if businesses rely too heavily on loans instead of improving cash flow systems.

3. Lulalend (South Africa)

Lulalend remains one of South Africa’s strongest fintech business lenders.

The platform focuses mainly on established SMEs with consistent revenue history.

Lulalend financing is commonly used for:

- Business expansion

- Inventory purchases

- Cash flow management

- Operational growth

Ideal for:

- Digital brands

- Retail chains

- Online businesses

- Growing service companies

4. M-KOPA Financing

M-KOPA has evolved beyond device financing into broader SME support across East Africa.

Many small retailers now use M-KOPA systems for:

- Inventory acquisition

- Retail equipment financing

- Business devices

- Operational tools

The platform’s integration with mobile money systems gives smaller businesses easier access to financing opportunities.

What Entrepreneurs Must Understand Before Taking SME Loans

One major mistake many business owners make is assuming loans automatically solve business problems.

In reality, financing only works effectively when a business already has:

- Stable demand

- Cash flow discipline

- Predictable sales

- Strong customer retention

- Clear profit margins

If these foundations are weak, borrowing can actually increase financial pressure.

For example:

A fashion retailer with strong monthly demand may use a ₦1 million inventory loan profitably during a high-sales season.

But another business with inconsistent sales may struggle to repay even a smaller loan.

This explains why many startups fail before profitability despite raising capital.

You can explore this challenge further here: Why Bootstrapped Startup Failure in Africa Is Getting Worse Before Profit (2026 Survival Guide).

Realistic Expectations About Online Business Financing

Many online discussions about fintech lending create unrealistic expectations.

Responsible entrepreneurs understand that:

- Small loans rarely create instant wealth

- Debt increases financial responsibility

- Cash flow matters more than loan size

- Business systems matter more than borrowed money

Short-term financing should be viewed as a temporary business tool, not a permanent solution.

This is especially important for beginners entering online business or side hustles.

Small income opportunities can help entrepreneurs learn:

- Marketing

- Customer service

- Financial management

- Digital sales systems

But long-term financial stability usually comes from building scalable digital assets.

Why Scalable Digital Assets Matter More Than Constant Borrowing

Many successful African entrepreneurs eventually shift focus away from repeated loan dependency toward building long-term digital income systems.

Examples include:

- Websites and blogs

- YouTube channels

- E-commerce stores

- Mobile apps

- Digital communities

- Email marketing systems

- Online marketplaces

Unlike temporary loans, digital assets can continue generating:

- Traffic

- Leads

- Customers

- Advertising revenue

- Affiliate income

- Recurring sales

The Valspill team increasingly helps entrepreneurs structure and develop these digital systems properly for sustainable monetization and long-term revenue growth.

How Small Loans Can Become Growth Opportunities

Smart entrepreneurs often use small financing opportunities strategically.

The progression commonly looks like this:

Stage 1: Starting a side hustle or local business

Stage 2: Learning customer acquisition and cash flow management

Stage 3: Using small loans responsibly for inventory or expansion

Stage 4: Building digital platforms that generate consistent traffic

Stage 5: Scaling through automation, systems, and recurring revenue

For example:

A small cosmetics seller may initially rely on inventory loans while selling products through WhatsApp. Over time, the business may evolve into a full e-commerce store with organic search traffic and automated payment systems.

This transition is explored further here: WhatsApp to E-Commerce Store: What Happened When I Moved My Small Business Online In 2026.

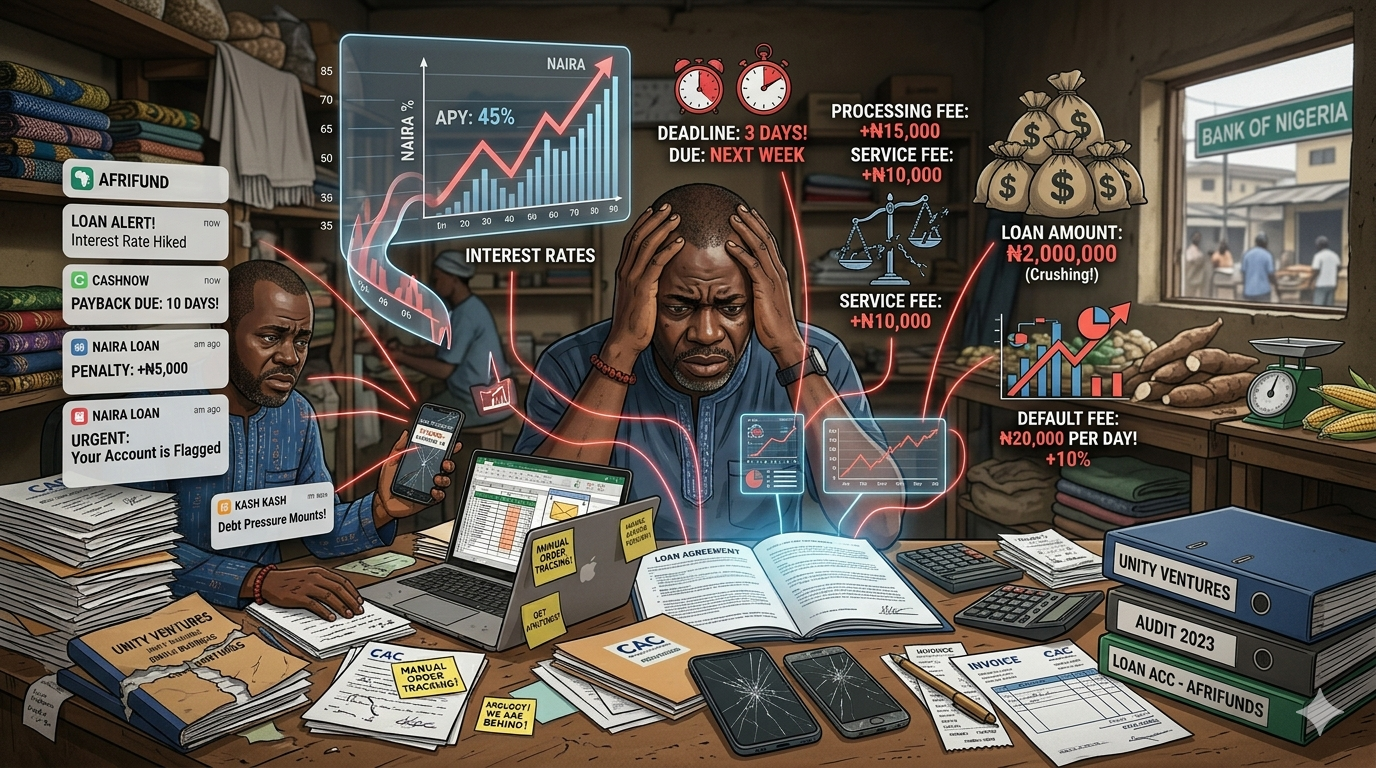

Hidden Costs Many SME Borrowers Ignore

Not every “low-interest” business loan is truly affordable.

Before accepting financing, entrepreneurs should examine:

- Processing fees

- Insurance deductions

- Late payment penalties

- Daily repayment structures

- Rollover conditions

- Hidden administrative charges

Some SME Loan Platforms In Africa advertise attractive monthly rates while the total repayment cost becomes significantly higher after fees are added.

Always calculate the full repayment amount before borrowing.

Alternative Funding Beyond SME Loan Platforms In Africa

Interestingly, many African entrepreneurs are now exploring funding systems outside traditional loans.

Alternative financing models include:

- Revenue-sharing partnerships

- Angel investors

- Supplier financing

- Crowdfunding

- Family office capital

- Strategic partnerships

In Nigeria especially, family office funding is quietly becoming a major source of private capital for growth-focused entrepreneurs.

This detailed guide explains the process: WhatsApp to E-Commerce Store: What Happened When I Moved My Small Business Online In 2026.

How SME Loan Platforms In Africa Are Reshaping Business Growth

SME Loan Platforms In Africa are no longer serving only informal traders.

Today, fintech lending supports:

- E-commerce startups

- Logistics companies

- Food businesses

- Creative agencies

- Agricultural suppliers

- Beauty entrepreneurs

- Freelancers and creators

As competition increases, many SME Loan Platforms In Africa are improving approval speed while lowering interest rates for businesses with strong repayment history.

This shift is helping more African entrepreneurs scale operations faster than traditional banking systems previously allowed.

Tax Structure And Compliance Still Matter

Many entrepreneurs underestimate how important tax structure and business compliance have become in modern fintech lending.

Lenders increasingly evaluate:

- Corporate registration

- Tax records

- Business banking activity

- Accounting systems

- Cash flow documentation

Businesses with stronger financial structure often gain access to:

- Larger loan amounts

- Lower interest rates

- Longer repayment periods

- Investor opportunities

This guide explains modern tax optimization strategies across Africa: Best Business Structure for Tax in Africa (2027 Tax Savings Strategy Guide).

Case Study: How A Small Ghanaian Business Used Fintech Loans Responsibly

In 2025, a small food distribution business in Accra reportedly began using short-term fintech financing to manage inventory purchases during high-demand periods.

Instead of borrowing aggressively, the owner focused on:

- Fast-moving products

- Predictable customer demand

- Short repayment cycles

- Inventory discipline

After stabilizing cash flow, the business expanded into:

- Online ordering systems

- Social media marketing

- Digital customer retention

- Website traffic generation

Over time, revenue became less dependent on emergency borrowing.

This is the long-term transition many successful SMEs eventually pursue.

Frequently Asked Questions (FAQ)

What are SME Loan Platforms In Africa?

SME Loan Platforms In Africa are digital lending services that provide financing to small and medium-sized businesses using fintech systems instead of traditional banking processes.

Are SME Loan Platforms In Africa safe?

Some platforms are regulated and transparent, while others may include expensive repayment structures or hidden fees. Entrepreneurs should research lenders carefully before borrowing.

Can startups without collateral get SME loans?

Yes. Many fintech lenders now use alternative credit scoring systems based on business transactions, mobile money activity, and digital payment records.

Which countries lead fintech SME lending in Africa?

Nigeria, Kenya, and South Africa currently dominate fintech business lending due to strong digital payment ecosystems and rising entrepreneurship activity.

Should small businesses rely completely on loans?

No. Loans should support growth strategically, while businesses focus on building sustainable revenue systems and scalable digital assets.

What is the biggest risk of fintech business loans?

The biggest risk is borrowing without stable cash flow. Businesses with weak revenue systems may struggle with repayment pressure and accumulating debt.

Final Thoughts

SME Loan Platforms In Africa are opening new opportunities for entrepreneurs who previously struggled to access business financing.

Fast approvals, digital applications, alternative credit scoring, and mobile accessibility are making it easier for small businesses to secure working capital in 2026.

Still, sustainable business growth requires more than access to loans.

The most successful entrepreneurs eventually focus on building:

- Strong customer systems

- Digital visibility

- Recurring traffic

- Scalable online assets

- Long-term revenue infrastructure

Ultimately, SME Loan Platforms In Africa can help businesses solve short-term cash flow problems, but lasting financial growth usually comes from building systems that continue generating customers and revenue long after the loan is repaid.

If you have used fintech business loans before, share your experience in the comments. What worked for your business, and what would you do differently?